With house prices falling at their fastest rate in more than a decade, real estate is a common point of discussion these days. Whether you are watching the news on TV, or reading the latest article on Stuff, the real estate economy is not being painted in a positive light. Talk commonly centres around the market downturn, market corrections, or even an impending housing crash.

However, the highs and lows of the market are all part of a normal business cycle. There will always be periods of economic growth, then periods of economic downturn. But it is important to remember that recession is part of this cycle, and it’s a natural progression to go through it.

As a professional Real Estate Agent, I see it as my responsibility to predict as accurately as possible where we are at in this cycle at any particular time. Our team here at Najib, and our clients depend of this advice so that they can prepare for what is going to happen, and then persevere during the tougher times.

In this article, I want to share my predictions with you, so that you have the knowledge to prepare and persevere as we continue to move through this correction period, and potential economic recession.

Following New Zealand’s first lockdown in 2020, we correctly predicted a sharp drop and a sharp recovery of the housing market. Then approximately 12 months ago, we highlighted that the housing “boom” we were witnessing was neither realistic, nor sustainable, and that this would lead to a negative impact on the industry.

More recently earlier this year, we predicted a 5 – 10% correction to the real estate economy, and this is evident in some regions across New Zealand now. Furthermore, I suggest that we will see a further total correction of around 15 – 20% in the coming months.

There is a direct correlation between the billions of dollars of “free money” – or “helicopter money” – that was printed by the Government as an intended cash boost to encourage spending post-Covid. Intended to stimulate the economy and the housing market, it meant that there was more disposable income, leading to more money being available to spend on “big” assets.

When there is a boom in the market, people become rich on paper, and stocks go up. Essentially, when there is money, the “rich” will spend it.

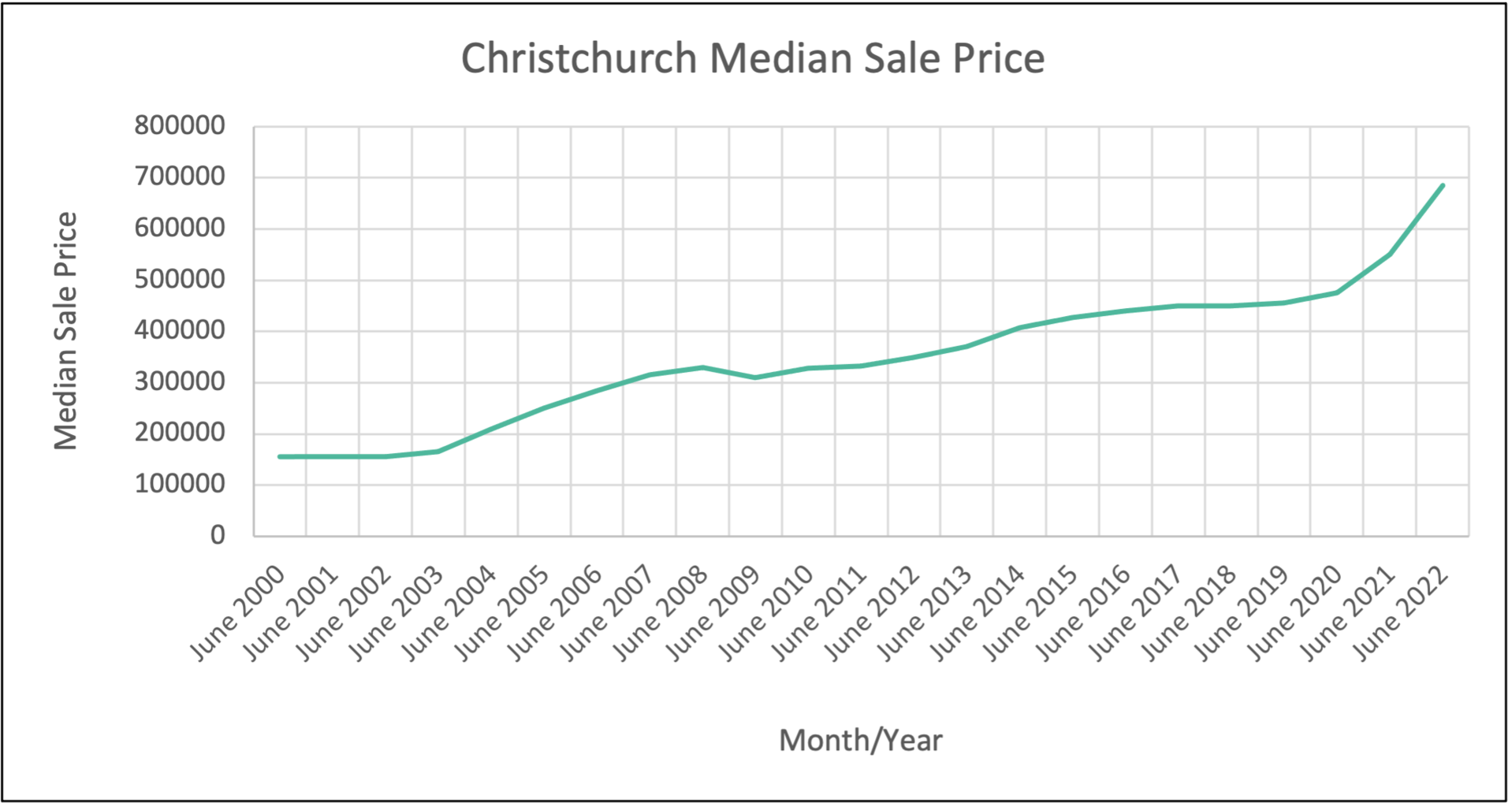

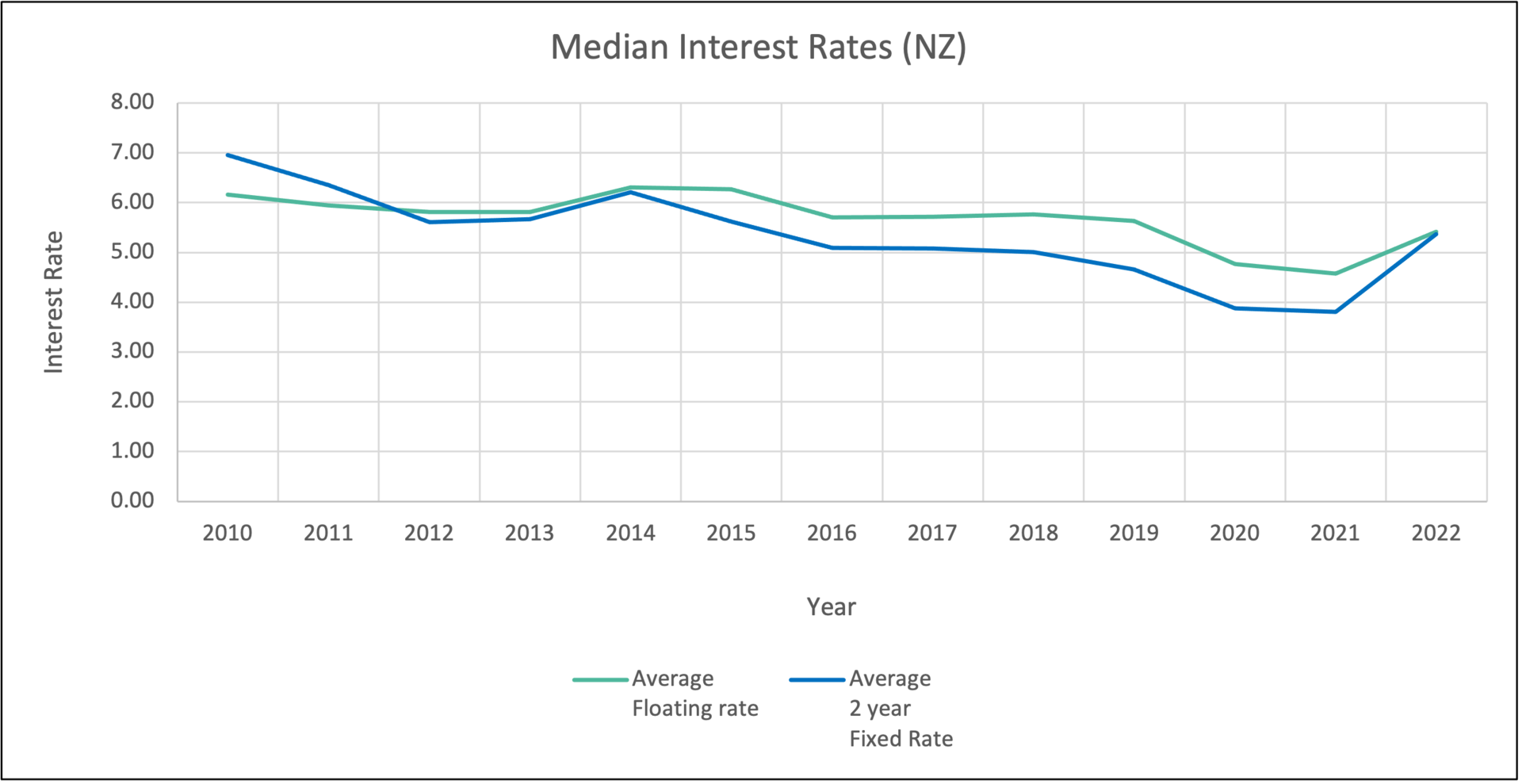

At the peak, things were looking great. From June 2017 to June 2022, the median house price in Christchurch increased by an incredible 52%. In 2021, we were experiencing historically low interest rates. Mortgage applications increased by 68% in the same period.

This led to a very strong sellers’ market. Less inventory contributed to soaring house prices as FOMO (Fear of Missing Out) took over buyers’ emotions.

However, 2022 has seen a turn in the housing economy. Interest rates are increasing (the average floating rate is now similar to what we saw in 2019,) and inflation has skyrocketed to 7.3% for the quarter to June 2022, due in part to rising construction prices and rental prices.

Construction material, transportation and labour costs have contributed to an 18 percent increase in the price for the construction of new dwellings (for the June 2021 to the June 2022 quarter.) The previous two quarters also showed 18% and 16% increases respectively.

When there is less disposable income, there is less money to spend. There tends to be an over-supply of inventory, house prices go down, and the market drops, moving us from a sellers’ to a buyers' market. Compounding this, rising interest rates also leads to property prices dropping, as consumers simply can’t afford the cost of a mortgage.

Unfortunately, there will be those who can no longer afford mortgage repayments. In such cases, this often results in massive price reductions, just so a property can be sold.

I am not here to spread fear, but I do believe that it is something that we should be prepared for.

As implied above, a huge factor in the housing market is affordability.

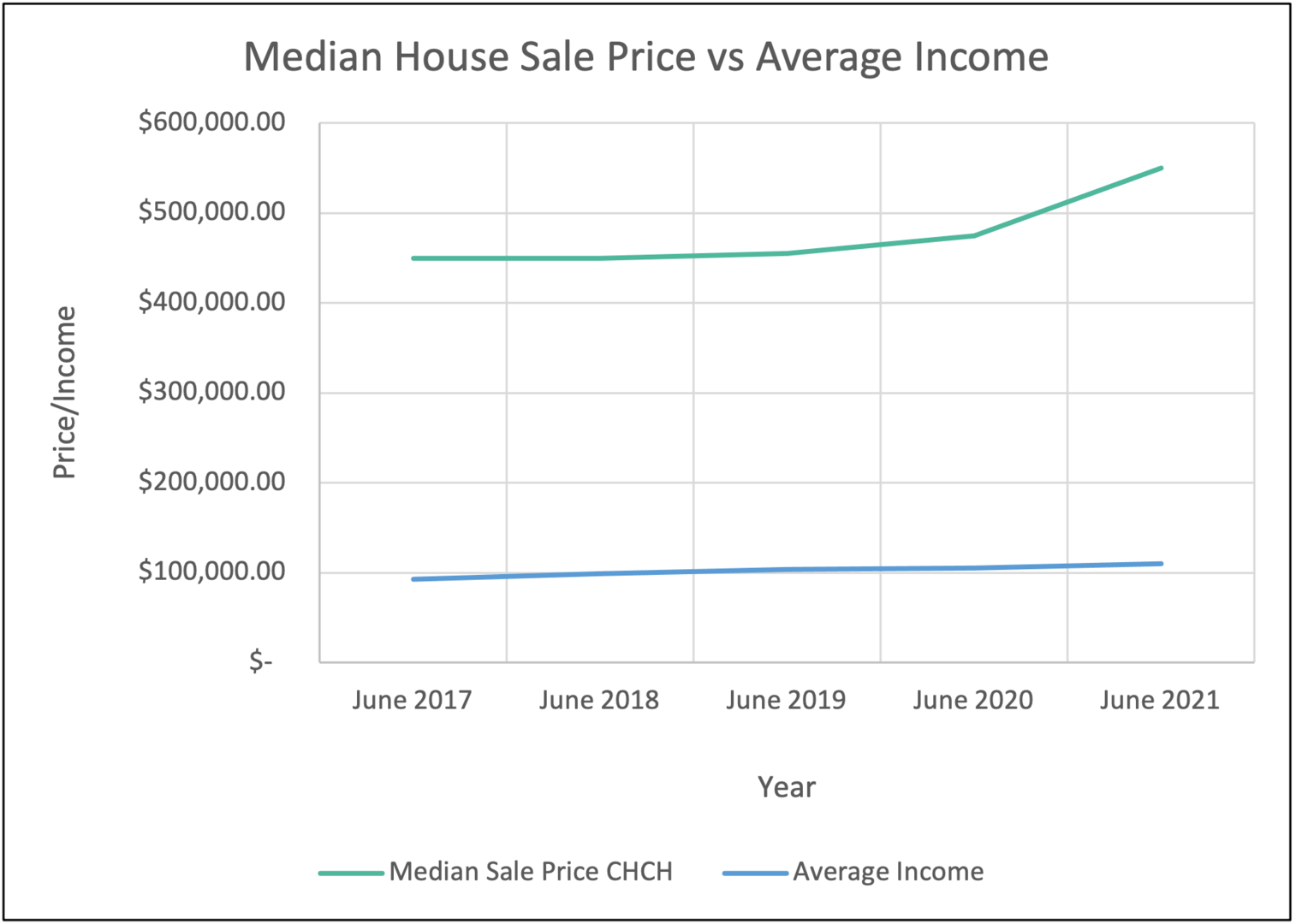

In June 2022, the average house price in Christchurch was $700,000, whilst the mean household income in 2022 is $117,774. This is nearly six times the average household income.

Whereas, affordable living is actually three to four times the household income. In both 2008 and 2017, for example, the price of a home in Christchurch was only 2 times the average household income.

For housing to become affordable once again, either salaries need to increase three-fold – or house prices need to come back. Although I’m sure many of us would love to see our pay package triple overnight, this is simply not going to happen.

Instead, to sell a home in a crowded buyers’ market, you have to lower your price. This is simply the economy of supply and demand.

If history is to repeat itself (as we know the economic cycle will) then this correction could become a “housing crash”, as more money has been printed this time than was before.

We want to share this knowledge with you so that you can predict, prepare and persevere. Although no one can 100% accurately predict the future, it is about giving you the best advice we can.

As always, if you would ever like to chat with us about your real estate options, do not hesitate to reach out to me directly or your Najib agent.