When it comes to OCR and mortgage rates in New Zealand, the biggest mistake most people make is trying to predict where rates are going next. Even economists get it wrong. And if you base your decisions on guesses, you can end up with a loan structure that does not fit your life when the real-world changes hit.

Instead, the better question is simple: If rates move up, am I positioned to handle it?

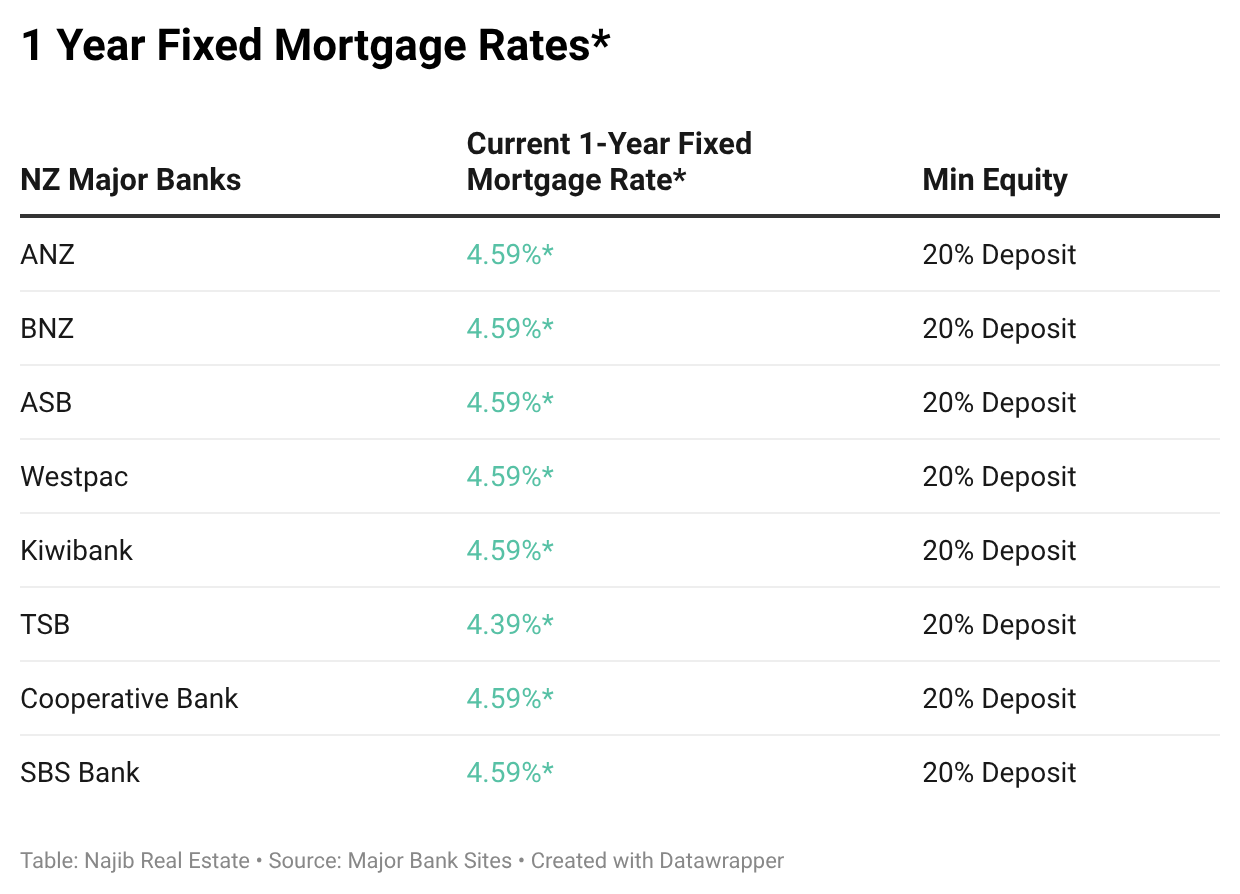

In our recent episode, we had Zhiyang Cheng, Top mortgage adviser in New Zealand from MHQ to share his insights about mortgage rates in 2026

Why the OCR matters (but forecasting doesn’t)

The OCR (Official Cash Rate) is a tool the Reserve Bank uses to control inflation. In general terms:

When inflation is high, rates tend to rise.

When the economy slows, rates tend to fall.

But here’s the practical point: you cannot control the OCR. What you can control is how you structure your mortgage, your cash buffers, and the level of flexibility you build into your repayments.

So don’t waste your energy asking “will OCR go up or down?” Ask “how do I structure my loan so I can cope either way?”

Don’t go on autopilot when you come off a fixed rate

A lot of homeowners treat fixed-rate maturity like a button press: the fixed rate ends, they go back to the bank, and they refix automatically. That is usually where people miss out.

- Your loan structure (is it still right for your goals and risk tolerance?)

- Cash flow (can you comfortably handle higher repayments?)

- Buffers (what happens if the “rainy day” arrives?)

- Rates might rise again: budget for the “what if”

- It is easy to get complacent when rates look low. But history shows rates can climb quickly. There have been periods where New Zealanders saw rates at 9%, and even higher in earlier years.

So if you are looking at your mortgage today, the mindset should be: “What if rates go to 5.5%, 6%, or even higher?” The correct response is not panic, it’s preparation.

Practical mortgage strategy for homeowners heading into 2026

One way to reduce risk is not to fix all your borrowing in one block. Splitting loans into different portions can help you manage uncertainty and keep options open.

For many people, an offset or revolving credit facility is one of the most useful tools in a higher-rate environment.

How it helps:

Interest reduction: if you keep savings in the offset/revolving account, that balance can reduce the interest you pay on the mortgage.

Access to your funds: unlike a term deposit, you typically keep flexibility and liquidity.

Lower “panic risk”: if repayments rise, having cash available makes it easier to stay comfortable.

A revolving credit facility can work like this: if you owe the bank $975,000 and you have $25,000 sitting in the revolving account, you can often avoid paying interest on that $25,000 portion while still keeping access to it.

Important: this only works well if you are disciplined. If you withdraw savings impulsively, the benefits disappear.

Lower rates feel great, but repayment confidence is what matters. You want to know your repayments still feel manageable if rates rise again.

Sometimes banks offer “cash back” or incentives for refinancing or staying. It is worth asking, and it is also worth comparing across lenders.

Working with a mortgage broker is not about “beating” banks with a magic rate. In fact, banks can be very competitive with rates.

The real value tends to be the advice piece and the structure of your lending. A bank employee generally follows the bank’s lending offer. A broker helps you work around your long-term goals, repayment strategy, and how you want to use property over time.

As one mortgage professional put it: banks can be quick for service, but they cannot (and should not) administer independent financial advice in the same way an advisor can.

A good broker will also consider things many borrowers overlook, such as:

- Loan structure fit for your risk tolerance

- Offset/revolving options for cash efficiency

- Whether you should float or fix portions of the loan

- How to position for your next purchase

There are two major ways revolving credit can be used.

A) Put your cash into revolving credit

If you have savings that would otherwise sit idle, using them in revolving credit can reduce the interest you pay.

B) Use equity top-ups, but only if you are disciplined

If you have equity, you can sometimes set up a revolving facility where you can access a pre-approved amount if needed. In some structures, interest is charged only on what you actually draw.

Why this matters for real estate: speed wins deals. If a great opportunity pops up and you need a deposit quickly, revolving access can make the difference between acting and missing out.

Simple mortgage structures can still save you money

You do not need complexity to get results. Many Kiwis use a basic split loan (fixed and/or floating). The key is not starting complicated. The key is reviewing regularly.

For example, if you initially put $25,000 cash into revolving credit and then your savings grow to $70,000 over the next year, you may need to adjust the structure to reflect your changed cash position. That is how you stop money from sitting idle and start using it to reduce interest.

Mortgage and property strategy does not change because you live in Auckland or Canterbury, but your numbers absolutely do.

Auckland typically has a higher entry cost, meaning:

- higher purchase prices

- often different rental yields

- more pressure on affordability

Canterbury often has a lower entry point and can offer higher yields, which can change how lending and rental cash flow work in practice.

Also, whether it’s owner-occupied or investment affects your strategy. Owner-occupied loans are generally not deductible in the same way, so the emphasis is often on paying down the loan sooner.

Banks are “open for business,” but investor appetite is different

A common question is how “friendly” banks are right now for lending. The answer is nuanced.

Banks have an internal credit policy and a test rate (a buffer above the loan rate used to assess whether you can afford repayments).

One key shift described recently is that after the toughest period (around 2021 to 2022), credit policy and test rate requirements eased somewhat. For example, test rates during the boom were roughly in the 5.8% to 6% range, while more recently borrowers may be tested around 6.5% to 6.8%.

So the problem is not necessarily bank appetite. The constraint is often investor affordability and sentiment:

prices can still be high relative to rental yield

investor rules and tax uncertainty can reduce confidence

yields may not cover costs as easily as they once did

Investing: capital growth matters, but cash flow keeps you in the game

For property investors, it is tempting to chase capital growth and ignore yield. But survival matters more than predictions.

If a deal has great long-term upside but weak yield, you might be forced to “top up” the mortgage from your own after-tax income. If your income drops, or rates rise, you may not be able to hold the property for the long run.

This is why cash flow is often the lifeline of an investment portfolio. It is also why banks focus heavily on serviceability and buffers.

And when it comes to scaling beyond one or two properties, serviceability becomes the bottleneck. Equity and cash flow are the two ingredients lenders look for most.

Even with house prices rising, first-home buyers should not assume they are “priced out” forever.

One important mindset shift: your first home is usually not your forever home. It is a stepping stone.

Key points to consider:

There are options such as low-deposit lending (for example, 5% deposit schemes, where eligible).

You might already have enough for a deposit if you have been saving.

Buy something with potential, not necessarily perfection. Some of the best entry properties do not look flash but can improve with time.

And try not to compare yourself to “Mr Jones’ son”. Different starting points are normal. Your job is to get a foothold, build equity, and plan your next move.

So what should you do next?

If you want a clear takeaway, it’s this:

Stop forecasting rates.

Start building resilience.

Review your fixed-rate strategy well before maturity.

Consider offset or revolving credit if it fits your discipline and cash flow.

Get tailored advice rather than defaulting to the same bank process every time.

Rates will move up and down, and the market will react. But if you structure your mortgage for stability, you give yourself the freedom to make smart decisions, not forced decisions.